A Supply Chain Forced Into Reinvention

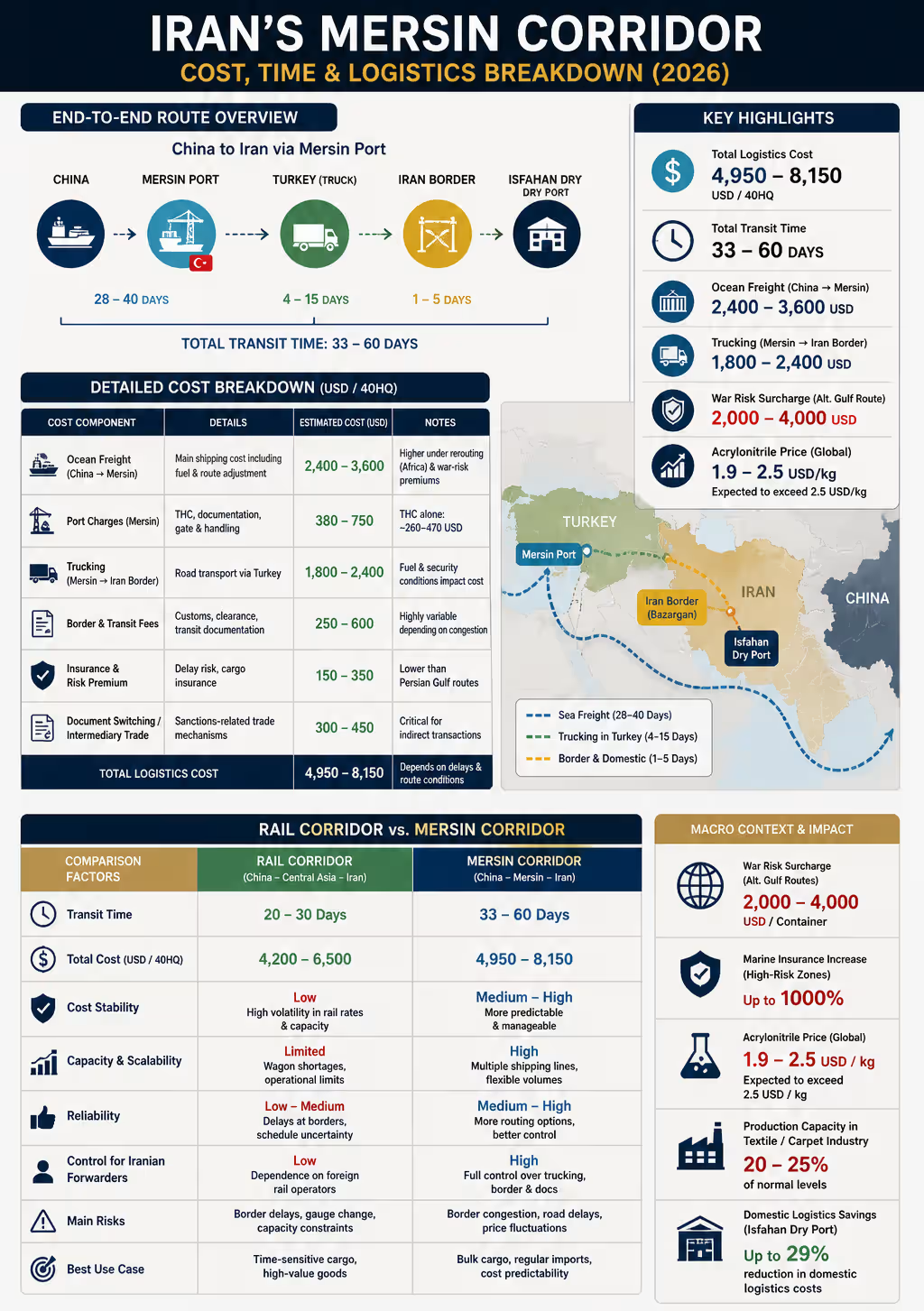

Iran’s trade system is no longer defined by efficiency metrics such as speed or cost optimization. Under escalating geopolitical pressure and the disruption of southern maritime routes, the country’s logistics architecture has entered a phase of forced reinvention. According to analysis published by the Isfahan Chamber of Commerce, the instability in Persian Gulf shipping lanes—combined with surging war-risk surcharges—has accelerated a structural shift toward alternative corridors, most notably via Mersin Port in Türkiye.

The magnitude of this shift becomes clearer when examining the cost distortions in traditional routes. War-risk surcharges alone have reached levels between $2,000 and $4,000 per container, while marine insurance premiums in high-risk zones have increased by several multiples. In practical terms, this has rendered southern routes not only expensive but operationally unpredictable.

Breaking Down the Mersin Route: Real Costs, Real Timelines

The Mersin corridor operates through a two-stage logistics chain: maritime transport from East Asia to the Eastern Mediterranean, followed by overland trucking into Iran.

The first stage—shipping from China to Mersin—now takes between 28 and 40 days under current conditions, compared to shorter pre-crisis benchmarks. Freight rates for a 40HQ container fluctuate between $2,400 and $3,600, depending on routing decisions, fuel costs, and insurance premiums.

Upon arrival, the second stage begins. Trucking from Mersin to the Iranian border typically costs between $1,800 and $2,400, while border handling, transit fees, and administrative costs add another $250 to $600. Insurance adjustments and delay-related risk premiums introduce an additional $150 to $350, and document switching or intermediary trade structures can add between $300 and $450 per shipment.

When combined with port-related charges—ranging approximately between $380 and $750 per container, including terminal handling, documentation, and gate services—the total end-to-end cost of the Mersin route reaches between $4,950 and $8,150 per 40HQ container.

Transit time, meanwhile, settles within a broad range of 33 to 60 days, depending largely on congestion at border crossings such as Bazargan.

Rail Corridor vs. Mersin: Speed Against Control

At first glance, the China–Central Asia–Iran rail corridor appears to offer a superior alternative. Transit times are typically estimated between 20 and 30 days, significantly shorter than the Mersin route. However, this advantage is undermined by structural constraints.

Rail capacity remains limited, with wagon shortages and dependence on foreign operators reducing scheduling reliability. Border crossings introduce further inefficiencies, particularly where gauge changes require cargo handling adjustments. As a result, while rail may deliver faster shipments in isolated cases, it lacks the scalability and predictability required for sustained trade flows.

The Mersin corridor, by contrast, offers a different form of value. Its cost may be comparable—or even higher in certain scenarios—but its operational control is significantly stronger. Iranian forwarders maintain direct influence over the inland segment, allowing them to manage risks more effectively despite longer transit times.

Hidden Costs and the True Price of Sanctions

What distinguishes the current logistics environment is not just the visible cost structure, but the accumulation of hidden expenses. The Isfahan Chamber analysis highlights that congestion, demurrage, and storage delays are becoming decisive cost drivers.

At the same time, global price dynamics are adding further pressure. The price of key petrochemical inputs such as acrylonitrile has approached $1.9 to $2 per kilogram, with projections suggesting a rise above $2.5/kg. This has direct implications for industries dependent on acrylic fibers, including Iran’s machine-made carpet sector.

In effect, companies are facing a dual burden: rising global input costs and increased logistical expenses driven by sanctions and geopolitical risk.

Read more: The Strategic Hub: Top 10 PVC Flooring Suppliers from Turkey for the MENA Market

Isfahan’s Role: Stabilizing the Internal Network

While external routes are under strain, internal logistics are being reinforced. The development of the Isfahan dry port—spanning approximately 729 hectares—has enabled a more centralized distribution model within Iran.

This inland hub has contributed to a reduction in domestic logistics costs by up to 29%, according to the same report. More importantly, it provides a controlled environment for storage and redistribution, insulating internal supply chains from the volatility of border regions.

In a fragmented external environment, this kind of internal consolidation becomes a critical stabilizing factor.

| Cost Component | Details | Estimated Cost (USD / 40HQ) | Notes |

|---|---|---|---|

| Ocean Freight (China → Mersin) | Main shipping cost including fuel & route adjustment | 2,400 – 3,600 | Higher under rerouting (Africa) & war-risk premiums |

| Transit Time (Ocean) | Shipping duration | 28 – 40 days | Up to 45 days in disrupted routes |

| Port Charges (Mersin) | THC, documentation, gate & handling | 380 – 750 | THC alone: ~260–470 USD |

| Trucking (Mersin → Iran Border) | Road transport via Turkey | 1,800 – 2,400 | Fuel & security conditions impact cost |

| Border & Transit Fees | Customs, clearance, transit documentation | 250 – 600 | Highly variable depending on congestion |

| Insurance & Risk Premium | Delay risk, cargo insurance | 150 – 350 | Lower than Persian Gulf routes |

| Document Switching / Intermediary Trade | Sanctions-related trade mechanisms | 300 – 450 | Critical for indirect transactions |

| Total Logistics Cost | End-to-end (China → Iran) | 4,950 – 8,150 | Depends on delays & route conditions |

| Total Transit Time | Full journey duration | 33 – 60 days | Border delays are key factor |

| War Risk Surcharge (Alt. Gulf Route) | Additional cost in southern routes | 2,000 – 4,000 | Major reason for route shift |

| Acrylonitrile Price (Global) | Key raw material for acrylic fiber | 1.9 – 2.5 USD/kg | Expected to exceed 2.5 USD/kg |

| Domestic Logistics Savings (Isfahan Hub) | Centralized distribution impact | Up to 29% | Based on dry port efficiency |

Industrial Impact: Pressure on Textiles and Carpets

The consequences of these shifts are particularly visible in sectors dependent on imported raw materials. Textile and machine-made carpet manufacturers are now operating under significantly tighter constraints.

Production capacity across many companies has reportedly fallen to 20–25% of normal levels, reflecting both supply chain disruptions and declining demand. Export markets in the Gulf region have weakened, while replacing nearby clients with distant markets introduces additional logistical and financial complexity.

At the same time, domestic demand has contracted sharply. Financing conditions have tightened to the point where many producers can no longer secure raw materials under deferred payment terms, further limiting production.

A New Regional Reality

As Iran’s trade system adjusts, regional supply dynamics are shifting. Markets that were once reliably served by Iranian producers are opening to alternative suppliers. Countries such as Türkiye, Pakistan, and others in the region are positioned to capture these gaps, particularly in sectors where continuity of supply is critical.

This is not simply a redistribution of market share—it is a structural change in how regional trade networks are configured.

Conclusion: The Cost of Continuity

The emergence of the Mersin corridor as a primary trade route reflects a broader transformation in Iran’s economic strategy under sanctions. The priority is no longer optimization, but continuity.

With total logistics costs reaching up to $8,000 per container and transit times extending beyond two months in worst-case scenarios, trade has become more expensive, slower, and more complex. Yet it continues—because alternative options are either unavailable or too risky.

In this environment, control has replaced efficiency as the defining metric of logistics. And for Iran, the Mersin route represents not just an alternative path, but the foundation of a new, more constrained economic reality.

{kind=link}